Share Buybacks: Weird News from Matt Levine

Oklahoma Oil and Gas Royalty Owners:

The always outstanding Matt Levine of Bloomberg, wrote great commentary on a recent Wall Street Journal piece about share buybacks in the oil and gas industry.

Matt quotes:

Laredo’s shares are trading more than 20% below what the company sold stock for in three offerings during the downturn.

snake_oil = "Public Equities" print (snake_oil)

Public Equities

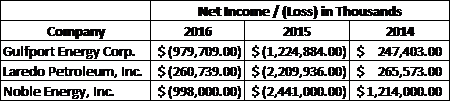

Noble Energy Inc. and Gulfport Energy Corp. are likely to buy at even bigger discounts to what they sold shares for in recent years. Noble said last week it would use proceeds from the sale of its Gulf of Mexico fields to repurchase $750 million of its stock, which is trading about 45% below the $47.50 its shares fetched in a $1.15 billion offering three years ago. Gulfport said it plans to buy back $100 million of the stock it sold at prices ranging from $21.50 to $47.75 in four offerings between April 2015 and December 2016. The Oklahoma City company’s shares ended Friday at $8.75.

and writes:

Don't get used to this! It is traditional to make fun of companies for buying high and selling low when they trade their own stock, but it is surely better than the alternative. After all, there is someone on the other side of those trades, and it's the shareholders. If companies could regularly raise money by selling stock when business was bad, and then buy that stock back more cheaply when business recovered, then what would be the point of investing in stocks?

Berlin believes that most public oil/gas equities are a hustle to begin with. SEC reporting requirements and metrics mislead the public about the health of the company. Net income for the companies mentioned above are captured in the chart:

Who likes losing massive amounts of money?

Why do folks buy shares of a company (who Berlin presumes actually want a claim on future profits and cash flows of that company) that sells its assets for less than it takes to replace them? Why continually throw money at a money losing enterprise where management incentives are so clearly misaligned from yours? A mystery to Berlin. Management lacks the skin in the game to promote reasonable governance. Berlin forecasts these managers blaming "capital markets" and "a shift in the macro-headwinds" before a mea culpa.

More to follow,

Berlin